What Are UAE Mortgage Rules in 2026?

UAE mortgage rules are regulated the UAE Central Bank and include LTV caps (75–80%), a maximum 50% debt burden ratio, minimum salary requirements, and tenure limits up to age 65–70.

Buying a home in the UAE is an exciting milestone, especially for expats. However, before stepping into the property market, it is essential to understand the mortgage regulations set the Central Bank of the UAE. These rules determine how much you can borrow, for how long, and under what conditions.

This guide explains the most important mortgage regulations — Loan-to-Value (LTV) ratios, mortgage tenure, salary requirements, and the Debt Burden Ratio (DBR) — in a clear, step--step way.

Quick Snapshot: UAE Mortgage Rules (2026)

Here’s a quick overview for expats and first-time buyers:

- Loan-to-Value (LTV): 80% max for first property (expats).

- Tenure: Max 25 years, up to borrower age 65 (salaried) or 70 (self-employed).

- Salary Requirement: AED 15,000–25,000 (typical minimum, varies bank).

- Debt Burden Ratio (DBR): Max 50% of net monthly income.

- Down Payment: 20%–25% minimum for expats (depending on property value).

Central Bank of UAE Mortgage Regulations Explained

Mortgage lending in the UAE is governed prudential regulations issued the Central Bank. These rules are designed to:

- Maintain financial stability

- Prevent over-borrowing

- Protect consumers from excessive debt

- Control real estate risk exposure

Therefore, all banks operating in Dubai, Abu Dhabi, and across the UAE must follow LTV caps and the 50% DBR rule.

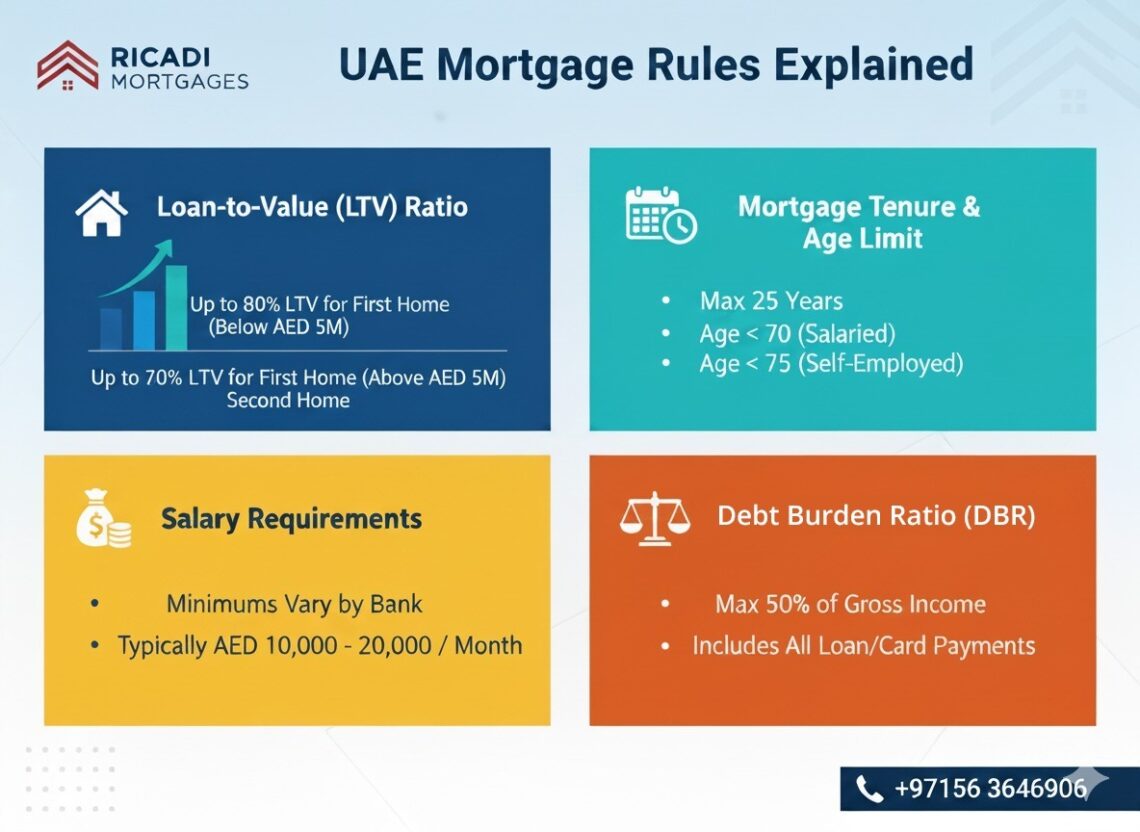

1. Loan-to-Value (LTV) Ratio

Definition:

LTV is the percentage of a property’s value that banks can finance.

For expats buying their first property under AED 5M, the max LTV is 80%.

If the property is above AED 5M, the LTV limit drops to 70%.

For second properties, it reduces further to 60%–65%.

Example:

If you buy a villa worth AED 2M, the maximum mortgage you can secure is AED 1.6M. The remaining AED 400K must be paid upfront as a down payment.

LTV Rules Breakdown (Expats vs Property Value)

| Buyer Type | Property Value | Maximum LTV |

|---|---|---|

| Expat – First Property | Under AED 5M | 80% |

| Expat – First Property | Above AED 5M | 70% |

| Expat – Second Property | Any value | 60%–65% |

2. Mortgage Tenure Rules in UAE

Definition:

Tenure is the maximum number of years you can repay your home loan.

UAE banks allow mortgage tenure up to 25 years. However, there is an age limit:

- Salaried expats: repayments must end before age 65.

- Self-employed expats: repayments must end before age 70.

Example:

If you are 45 years old and salaried, your maximum tenure is 20 years (until age 65).

Maximum Mortgage Age Limits

| Employment Type | Maximum Age at Loan Maturity |

|---|---|

| Salaried | 65 years |

| Self-Employed | 70 years |

3. Salary Requirements for UAE Mortgages

Definition:

Salary requirement refers to the minimum monthly income needed to qualify.

Banks generally expect AED 15,000–25,000 monthly income for expats.

Some lenders may accept AED 12,000 for smaller properties. Premium banks may require AED 25,000+.

Eligibility also depends on:

- Employer category

- Length of employment

- Credit score

- Existing liabilities

Example:

A salaried professional earning AED 20,000 with no debt may qualify for an AED 1.5M–1.8M mortgage.

4. Debt Burden Ratio (DBR) – The 50% Rule

Definition:

DBR is the percentage of your Net Monthly Income (NMI) that can go toward debt repayments.

As per UAE Central Bank guidelines:

Maximum 50% of your NMI can be used for total debts.

This includes:

- Mortgage installment

- Car loans

- Personal loans

- Credit card minimum payments

DBR Formula

DBR = (Total Monthly Obligations ÷ Net Monthly Income) × 100

Example Calculation:

NMI = AED 25,000

Existing debt = AED 3,000

DBR limit = 50% × 25,000 = AED 12,500

Available for mortgage = 12,500 – 3,000 = AED 9,500

This means your mortgage installment cannot exceed AED 9,500 per month.

You might be interested to know – Best Mortgage Rates in UAE

Mortgage Rules in Dubai vs Abu Dhabi

Mortgage regulations are federal and apply across the UAE. Therefore, LTV caps and DBR rules are consistent in:

- Dubai

- Abu Dhabi

- Sharjah

- Other Emirates

However, processing standards, valuation policies, and bank preferences may vary slightly depending on the property location and developer profile.

Quick Reference Table: UAE Mortgage Rules (2026)

| Rule | Details (Expats) | Example |

|---|---|---|

| Loan-to-Value (LTV) | 80% up to AED 5M; 70% above AED 5M | AED 2M villa → AED 1.6M mortgage |

| Tenure | Max 25 years; end age 65/70 | 45 y/o salaried → 20 years |

| Salary Requirement | AED 15K–25K typical | AED 20K income → ~AED 1.5M loan |

| Debt Burden Ratio | Max 50% of NMI | NMI 25K, debt 3K → 9.5K available |

| Down Payment | 20%–25% minimum | AED 2M home → AED 400K upfront |

FAQs on UAE Mortgage Rules

1. Can expats get 100% mortgage in the UAE?

No. Expats must make a down payment of at least 20%–25%, depending on property value.

2. What is the maximum mortgage tenure in Dubai or Abu Dhabi?

25 years, subject to age limit (65 salaried / 70 self-employed).

3. Does credit score affect mortgage approval in the UAE?

Yes. Most banks check your AECB credit score before approving.

4. What is the maximum LTV for second property in UAE?

Typically 60%–65%, depending on bank and borrower profile.

5. Can I get a mortgage with AED 10,000 salary in UAE?

Some banks may consider applications around AED 12,000+, but eligibility depends on DBR and existing obligations.

6. What is the 50% mortgage rule?

It refers to the Debt Burden Ratio cap where total debt obligations cannot exceed 50% of net monthly income.

7. What is the maximum age limit for mortgage in UAE?

65 for salaried borrowers and 70 for self-employed.

8. Are mortgage rules different for off-plan properties?

LTV limits generally apply, but additional developer and escrow considerations may exist.

Why Work With Ricadi Mortgages?

UAE mortgage rules can be overwhelming. However, with Ricadi Mortgages, you don’t have to navigate them alone.

Ricadi Mortgages are the expert consultants in Dubai – Learn more

We specialize in expat mortgages across Dubai, Abu Dhabi, and beyond.

Our experts simplify LTV, DBR, and bank policies to secure the best possible deal.

From eligibility checks to bank negotiations, we manage the process end-to-end.

Call us today: +971 56 364 6906

Visit: www.ricadimortgages.com